The report “UAE Free-Zone Betrayal 124 Corporate Enablers Defying US Sanctions on Russia and Iran” published by Independent UN Watch, argues that Dubai’s free zones have become the operational backbone of a large?scale sanctions evasion system serving both Russia and Iran, rather than a collection of isolated compliance failures.

The report documents more than 120 UAE-linked firms that transform U.S. and EU sanctions from binding constraints into manageable transaction costs, sustaining billions of dollars in revenue for Moscow and Tehran.

Sanctions Landscape: Tools on Paper, Loopholes in Practice

The analysis is grounded in U.S. sanctions authorities administered by Office of Foreign Assets Control, particularly Executive Orders 14024 (Russia), 13846 (Iranian petrochemicals), and 13902 (Iranian ports and oil sector), alongside G7 oil price caps and parallel EU and UK measures. These regimes are designed to block assets, restrict dollar clearing, and impose secondary sanctions on non-U.S. facilitators.

From 2023 through early 2026, repeated OFAC actions involving UAE-linked firms and vessels revealed the Emirates not as a peripheral risk but as a recurring conduit. Approximately 12 percent of global shadow-fleet tanker calls involve UAE ports such as Jebel Ali and Fujairah. Despite more than 120 Russia-related OFAC designations and dozens targeting Iranian petrochemical networks, intermediaries in UAE free zones continue exploiting weaknesses in beneficial-ownership registries and trade-based money-laundering controls.

UAE as a Central Evasion Hub

The study identifies the United Arab Emirates—particularly Dubai—as a strategic node in a hybrid Russian-Iranian sanctions-evasion architecture. Free zones such as Dubai Multi Commodities Centre and Dubai International Financial Centre are characterized as structurally high-risk due to high license volumes, short-lived shell companies, nominee directors, and fragmented regulatory oversight.

DMCC alone issues thousands of licenses annually, many to entities that dissolve within six to twelve months, while DIFC’s wealth-management ecosystem adds opacity to dollar transactions and cross-border investments. Although the UAE exited the FATF grey list in 2024, the report argues that vulnerabilities persist in gold trading, telecoms, and beneficial-ownership thresholds.

Network behavior shows design rather than coincidence: most Tier-1 and Tier-2 firms share overlapping addresses, while Tier-3 entities cluster around generic “general trading” labels commonly linked to trade-based money laundering. Ports such as Fujairah host frequent ship-to-ship transfers involving tankers that disable AIS and blend sanctioned crude before onward shipment.

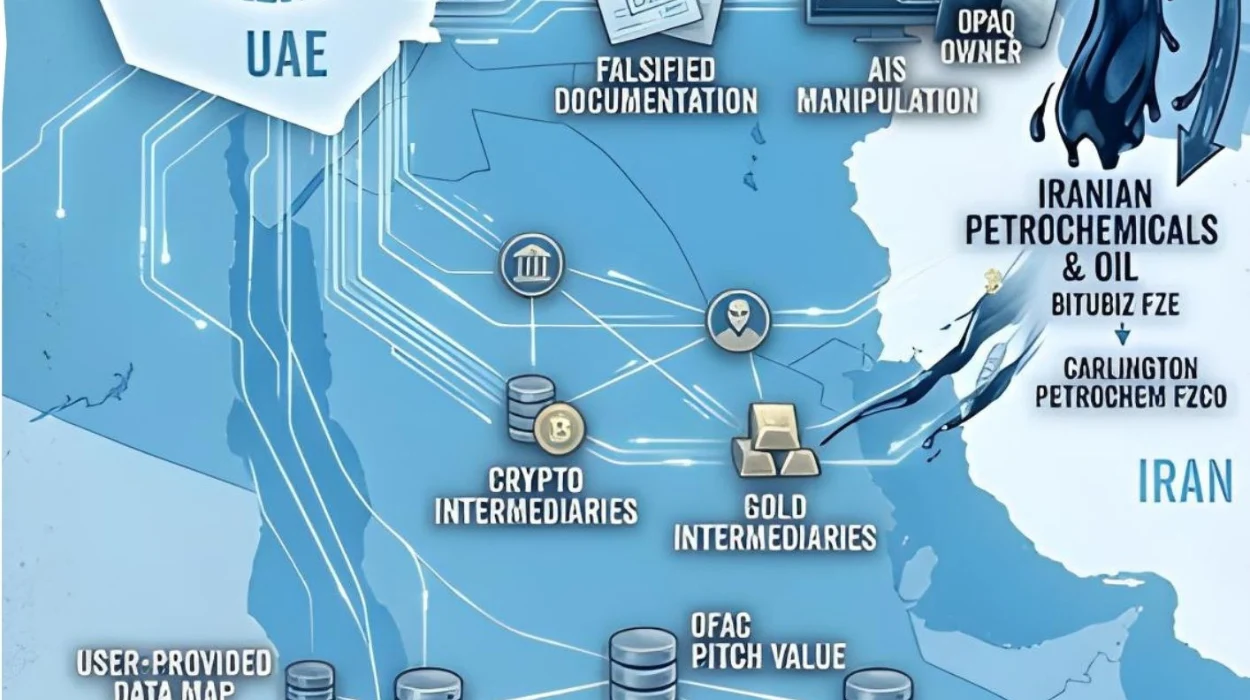

Corporate and Operational Architecture

Russian-linked networks center on Dubai-based oil traders and surrounding shell companies that share addresses, directors, and tanker pools, enabling price-cap breaches through opaque ownership and shipping practices.

Parallel Iranian networks rely on firms that falsify shipping documentation and misdeclare petrochemical cargoes, allowing Iranian oil and petrochemical revenues to pass through customs and financial systems as non-Iranian trade. These logistics and trading layers are linked to Iran’s Ministry of Defense and Armed Forces Logistics (MODAFL), channeling revenues into global markets through UAE shells.

Corporate service providers industrialize the system by creating and rotating anonymous special-purpose vehicles. Investigations and leaked records show that some formation firms marketed structures explicitly designed to circumvent sanctions using threshold manipulation and rapid corporate turnover.

Maritime managers form the operational arm of the shadow fleet through flag-hopping, opaque ownership, and AIS manipulation. Financial intermediaries in crypto and gold convert restricted revenues into portable wealth, while real-estate SPVs absorb high-risk funds into luxury property developments in Dubai Marina, Palm Jumeirah, and other prime districts.

Sectoral Concentration of Risk

Quantitative mapping shows concentration across key sectors:

- Oil and petrochemical trading (?61%) – responsible for an estimated USD 6.2 billion in illicit flows between 2023 and 2026.

- Maritime management and shadow fleet (?20%) – enabling more than 500 high-risk port calls annually.

- Gold and precious metals (?10%) – laundering roughly 19 tonnes of bullion per year.

- Crypto brokerage and OTC liquidity (?5%) – moving over USD 500 million through lightly regulated desks.

- Corporate service providers (?4%) – generating more than 1,200 shell entities annually for high-risk clients.

- Real estate and trade-based money laundering vehicles (?10%) – channeling roughly USD 3 billion into property and TBML schemes.

Across these sectors, repeated fingerprints emerge: shared addresses, recycled nominees, short corporate lifespans, and sequential sectoral roles supporting an estimated USD 10–15 billion in sanctions-evasion flows.

Case Illustrations

Selected cases demonstrate the mechanics of the system. A Sharjah-based terminal operator was sanctioned for inflating revenues through sham contracts linked to Iranian interests, using falsified documentation and circular transactions. Corporate service providers exposed in leaked financial records facilitated offshore structures for oligarchs and Iranian actors tied to shadow-fleet operations. Crypto-to-cash networks combined digital asset conversion with gold trading to obscure financial trails after physical commodity transactions.

These cases reinforce the conclusion that the infrastructure reflects knowing intent to evade sanctions rather than accidental compliance failures.

Regulatory Gaps and Strategic Risk

The report criticizes limited enforcement and administrative fines as inadequate against billion-dollar incentives. Weak beneficial-ownership verification, free-zone autonomy, and inconsistent oversight are identified as systemic drivers of risk. Although secondary-sanctions pressure has reduced some flows, the system adapts by shifting value into crypto, gold, and real estate.

Strategically, the authors argue that this infrastructure directly undermines U.S. national security objectives by financing Russia’s war in Ukraine and Iran’s missile and regional military programs.

Policy Recommendations

The report calls for network-centric enforcement rather than incremental name-by-name designations. Key recommendations include:

- Targeting core Tier-1 entities for SDN listings and secondary-sanctions warnings.

- Conducting focused reviews of maritime and crypto actors to support shipping advisories and asset freezes.

- Issuing sector-wide advisories on DMCC commodity shells and unlicensed crypto brokers.

- Coordinated U.S. actions involving DOJ subpoenas, FinCEN geographic targeting orders, and diplomatic pressure tied to FATF compliance.

- UAE-specific reforms such as lowering beneficial-ownership thresholds, suspending high-risk free-zone licenses, and restricting port access for non-transparent tankers.

Proposed benchmarks include securing 25 new SDN listings within 90 days and reducing shadow-fleet port calls by 40 percent within six months.

The study frames the UAE free-zone system as a test case for the credibility of modern sanctions regimes. By mapping more than 290 companies into over 20 coordinated sub-networks, it demonstrates that shared addresses, recycled directors, and short-lived shells constitute structural evidence of intent.

Failure to confront this architecture risks emboldening other evasion hubs and prolonging conflicts in Ukraine and the Middle East. A rapid, network-focused OFAC response targeting UAE-based facilitators could dismantle key nodes, restore sanctions integrity, and signal that free-zone opacity will no longer serve as a safe harbor for state-sponsored sanctions evasion.